Back in 2018 it was pretty clear that the IRS Automated Collection Systems (ACS) was stalled. What's happening in collections now? What meaningful external events can motivate you to resolve your tax problem?

Passport Renewals Are Stopped on 50k plus debts. If you owe more than $50,000 to the IRS and you haven't worked out an installment agreement, Offer in Compromise or Currently Not Collectible, you should expect passport renewals to fail. We find passport-blocks particularly on cases where the tax liability is nearly expiring (!).

Automated Collection Systems Dormant Again (With Exceptions). IRS letters are going out BUT there is little enforcement/levies just as was the case from January 2016 to Summer of 2018. However, if you have a liability that is nearly expiring, we see a heightened risk for wage levies/bank levies from ACS.

Revenue Officers Still Collecting But Overworked/Backed Up. If you owe more than $250,000 to the IRS or owe a five-figure plus amount of 941 - Payroll Taxes, you should expect a Revenue Officer to see your case. But cases aren't getting assigned to ROs quickly and when they are assigned, the case inventory is burdensome and ROs are not super quick to levy or in processing the "resolution" of your case.

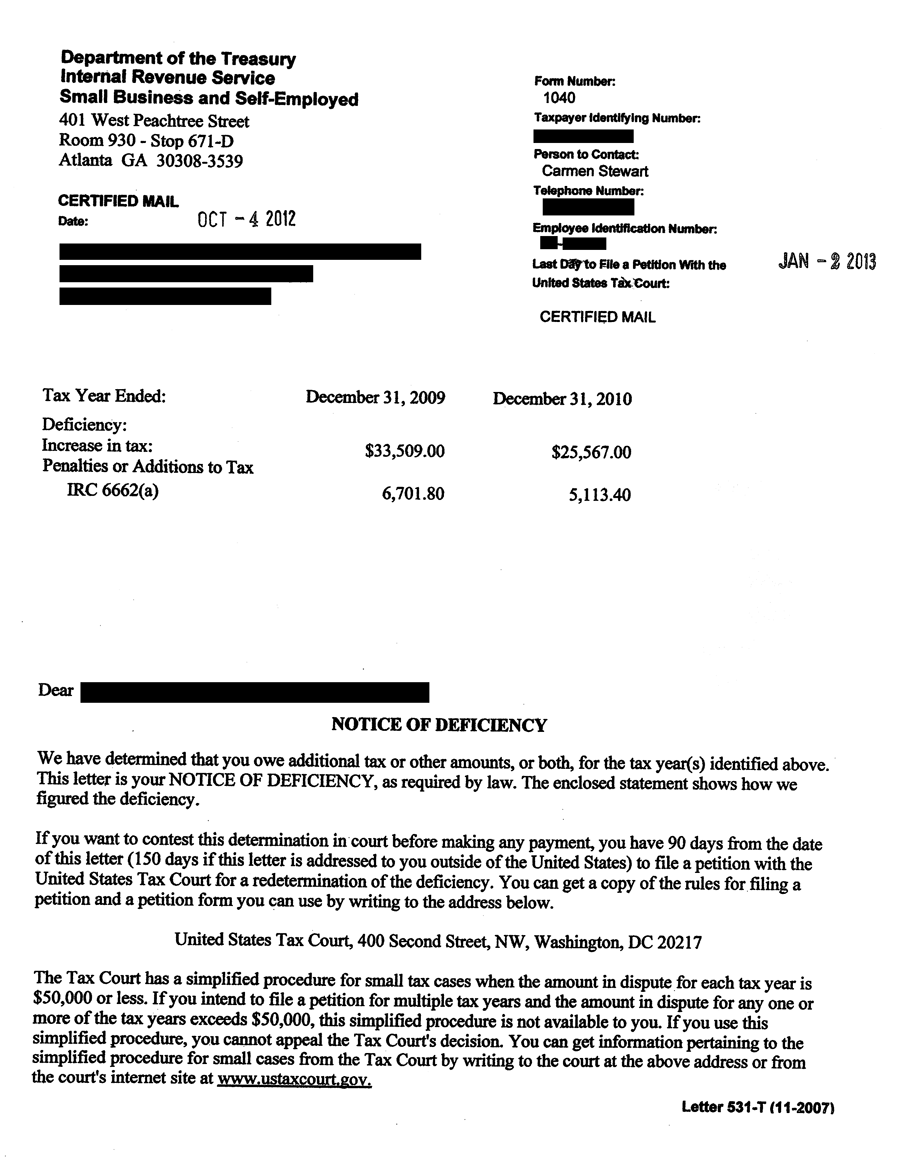

Non-Filers of Returns Getting Contacted. If you haven't filed taxes in a few years, IRS will prepare your return for you and assess the tax debt. You'll get a Proposed Assessment Letter or CP2000 and then a Notice of Deficiency. You'll be able to "replace" the IRS filing for you, BUT you'll want to do this fairly quickly to avoid getting stuck in IRS bureaucratic delay.

Audits of Non-Filers and Egregious Returns Still Happen Live, "in-your neighborhood" audits are still happening this summer, particularly when you haven't filed a lot of returns with potentially large income OR if you filed an egregious return, for example, using the Employee Business Deduction (now retired in 2018) on your Schedule A while also reporting losses on a Schedule C (!).

Homebuyers Still Need Tax Returns. If you are looking to buy a house, you'll still need to file at least your two or most recent years to comply with your lender.

{kind=link}

{kind=link}